|

| For a Better Tunghai |

|

| For a Better Tunghai |

Learning to accept and embrace market volatility

學習接受並掌握市場波動

by Charles Cheng, CFA – Clarity Investment Partners

鄭又銓, CFA -可承資本

The average investor in stock markets around the world has had a rough 2015 so far. The MSCI World Index of developed markets was down -7.5% YTD as of the end of September. The US S&P 500 was down -6.7%, the Hong Kong HSI index down -11.7%, and the TAIEX Index was down -7.9%. From the year’s high to the end of September, the US, HK, and Taiwan markets are down -10%, -24% and -13.5% respectively. These losses can be enough to make some investors fearful of putting too much of their savings in the financial markets, but even these pale in comparison to those suffered in the global financial crisis of 2008. However, being under-invested can be a much costlier mistake.

迄今為止,2015年對於投資全球股市的一般投資者都是艱難的一年。由今年初至9月底,已開發市場的MSCI指數下跌了7.5%,美國標準普爾500跌6.7%,香港恆生指數跌11.7%,而台灣加權指數下挫7.9%。從年中高點至9月底,美國、香港以及台灣股市分別下跌10%,24%以及13.5%。儘管今年的下跌與2008年全球金融危機相比可謂小巫見大巫,但是這些損失已經足以使一些投資者害怕將其存款投入資本市場。然而,投資不足卻可以是更昂貴的錯誤。

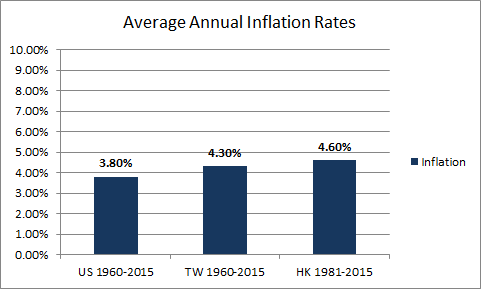

In the long term, the gain or a loss in a single year does not matter as much as consistent returns over time. On average over the past century or several decades, inflation around the world has roughly been around 4%. From 1960 to present day, US inflation averaged around 3.8% and Taiwan inflation around 4.3% (HK 4.6% since 1981). At these rates, even a 30% gain on the total amount of one’s assets in a single year would be wiped out in purchasing terms within seven to eight years if the assets did not continue to be invested for a return.

從長遠來看,隨著時間的推移,單一年度的收益和虧損與長期的穩定回報相比並不重要。在過去一個世紀或幾十年,全球各國的通脹平均值約為4%。從1960年至今,美國的通脹平均值約為3.8%,台灣為4.3%(香港自1981年至今通脹平均值為4.3%)。按照這些通脹速率,如果資產沒有持續的得到再投資,即使在一個單一年度的回報達到30%,這些回報也會在七至八年中被通脹逐漸消耗。

Chart 1: Average historical inflation rates around 4%

表1: 平均歷史通脹值為約4%

Source: Trading Economics

來源:Trading Economics

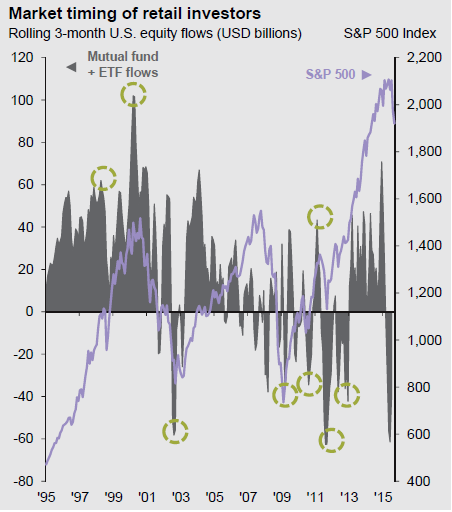

While real estate investments provide somewhat of a hedge against inflation, liquid investments are also a key component to preserving wealth. However, for the average investor, financial markets tend to be extremely difficult to time, especially if one is moving in and out of their positions frequently. Research shows that flows into mutual funds are the highest during market peaks, and fewest during market lows, exactly the opposite result from good timing. Often, people are willing to take a lot of market risk after markets have gone up for a while, and completely unwilling to take risks if the markets have entered a prolonged slump. If they are too fearful or hurt due to a market decline they may never get back into the market, leading to permanent loss. These tendencies makes it difficult for many investors to enjoy consistent returns.

儘管房地產投資在某些程度上對通脹具有一定對沖作用,投資於流動性資產卻是資產保值的一個重要組成部分。然而,對於一般投資者,特別是進出市場較頻繁說時,是很難去判斷資本市場的最佳投資時機。研究顯示,在市場的巔峰時投入共同基金的資金最多,而在市場低迷時的投資資金最少。這個模式與良好的進場時機正好相反。通常,人們在市場上漲一段時間後才開始願意承擔大量市場風險,卻不願在市場已經進入一段長時間低迷狀態後冒風險。如果由於市場下跌使得這些投資者太害怕或損失太慘重,他們也許永遠不會重新進入市場,並導致永久虧損。這樣的投資模式使投資者很難擁有穩定的回報。

Chart 2: Investors tend to get in and out at the worst times

表二:投資者往往在最差的時機進出市場

Source: JP Morgan, Guide to Markets Asia 4Q 2015

來源:摩根大通,亞洲市場指南2015年4季度

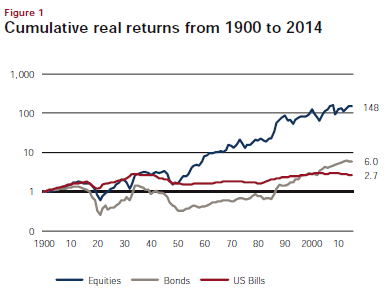

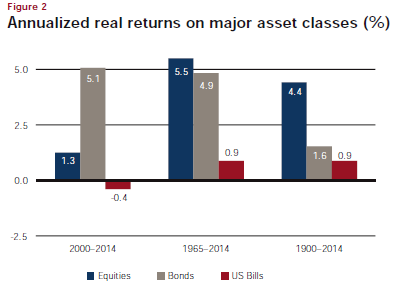

The good news is that global financial markets provide an avenue for such returns, provided that one’s investment horizon is long enough, and have the ability to stay within a consistent and diversified investment plan. In Chart 3 below, we see that the combined securities markets around the world have outpaced inflation for over the past 100 years. Global markets have persevered through major wars and disasters due to continuing economic growth through capital formation and technological progress. Equities have had the highest return of all major asset classes since 1900, with the combined equity markets returning an annualized 4.4% over inflation, while bonds have returned an annualized 1.6% over inflation.

好消息是,如果一個投資者的投資期限足夠長,且能夠保持一致且多元化的投資計劃,那麼全球金融市場將對獲得這樣穩定的回報創造有利條件。 從下文的表三我們可以看到,如果把世界各地的證券市場合併來看,在過去的100年,其回報是跑贏通脹的。資本的形成以及技術的進步使得經濟持續增長,這使得全球金融市場得以在經歷過重大戰爭及災難後依舊欣欣向榮.自1900年至今,在所有主要資產類別中股票的投資回報最高。把全球股市合併來看,其年化回報在扣除通脹率後為4.4%,而債券的年化回報為扣除通脹後1.6%。

Having a mix of asset classes also helps to make the returns more consistent over time, as in the most recent period covered, from 2000-2014, global bonds have returned 5.1% over inflation while equities returned 1.3%. It’s worth noting that the real return of equities was still positive despite the period starting with and including two of the biggest global stock market crashes ever. Starting from 1900, an investment in the global equity markets would have increased by 148 times by 2014 even after taking into account inflation.

擁有不同資產類別的投資組合也能幫助在長期投資中獲得較穩定的回報。自2000至2014年,全球債券回報率在扣除通脹後為5.1%,而同樣的時期,股票的回報率為1.3%。值得一提的是,儘管上述的時間段的伊始以及中間經歷了最大的兩次全球股市股市崩盤,股票的實際回報依舊是盈利的。而由1900年至2014年,全球股市的回報率,在扣除通脹後為148倍。

Regarding individual countries, certain markets have outperformed the combined global markets for certain stretches of time, but tend not to have such outperformance last over all time horizons. For example, the stock markets of Taiwan and Japan outperformed global averages significantly until 1990 and then subsequently underperformed. The most consistent outperformer has been the US equity market, but even then, there is no guarantee that it will continue. Having a broad mix of countries tend to smooth out much of the boom and bust characteristics of individual markets, despite most countries being simultaneously affected during financial crises.

在某些時期,某些個別國家的金融市場表現超越了全球整體市場回報,但並非在所有時間跨度都有如此出色表現。舉一個例子,台灣與日本的股市在1990年前都跑贏全球股市平均水平,然而之後該兩國股市表現卻遠遠不及其他市場。美國市場在過去曾經穩定的跑贏全球股市,但即使如此,無人可保證這將持續下去。儘管大部分國家的股票市場在全球性金融危機中都會同時受到影響,但是在資產分散投資於不同國家的股市可能使資產組合受到個別市場在特定時期的大漲與大跌的衝擊降低。

Chart 3: Global financial markets have well outpaced inflation for over 100 years

表3:全球金融市場已經跑贏通脹超過100年

Source: Credit Suisse Global Investment Returns Yearbook 2015

來源:瑞信2015全球投資回報年鑑

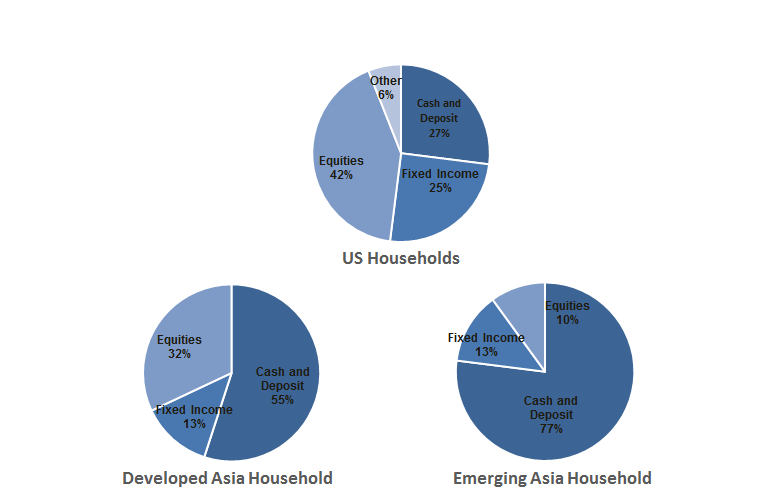

Have investors been taking advantage of these returns? According to a survey done in 2014 (figure 1), investors in Asia tend to under-allocate to financial investments in their portfolios, versus Western countries like the United States. Taking into account all financial securities excluding cash, Asia households only invested 23%-45% of their portfolios, holding the remaining 55%-77% in cash and deposits, versus 73% in the US, with 27% remaining in deposits. With deposit rates now returning below the inflation rate, that small proportion of equities and bonds in Asian portfolios is not sufficient to even keep pace with inflation, assuming returns follow the historical patterns.

那麼投資者們是否利用了這些回報?根據2014進行的一項調查顯示(圖1),亞洲的投資者與西方國家,如美國的投資者相比,前者在其投資組合中較少配置金融類投資項目。除了現金以外的所有金融證券類投資類別,亞洲家庭只拿出其投資資產中的23%-45%投資於金融證券,而其餘的55%-77%為現金或存款。而美國家庭投資於金融證券比例高達73%,存款為27%。鑑於目前存款利率低於通脹率,假設收益模式按照歷史數據,那麼亞洲家庭用少部分資金投資於股票與債券是不足以跟上通貨膨脹。

Chart 4: Asian Households tend to be underinvested in financial markets

表4:亞洲家庭往往在金融市場投資不足

Source: JP Morgan

來源:摩根大通

In conclusion, investors, especially in Asia, should learn to accept and embrace market volatility as a prerequisite for beating inflation and preserving wealth. Often, advice from financial advisers or bankers leaves households with too small a portion of their assets and in too risky or concentrated investments with a possibility of permanent loss because they do not have these long term objectives in mind. In the US and Europe, households have shifted towards managing assets completely independent from advice of commission based brokers and bankers or towards discretionary managers who have more aligned interests. Investors should seek to broaden their knowledge of financial markets not only in their home country, but around the world, and adopt a disciplined plan to remain consistently invested through most market environments, either by themselves, or with the help of a dedicated investment manager.

綜上,投資者,尤其是亞洲的投資者們,應該學會接受並掌握市場波動,作為對抗通貨膨脹以及資產保值的先決條件。一般情況下,財務顧問或銀行業者因其沒有考慮到長期目標這一因素,所以他們提供的投資建議會使一般家庭投入過小部分資產到風險過高或可導致永久虧損的集中投資裏。在歐美國家,一般投資人已經普遍將投資管理從基於佣金的經紀人或銀行業者手中交由全權委託式的資產管理機構,因其與客戶能更大程度上保持利益一致。投資者應尋求開闊其對不同金融市場,包括其本國的以及其他國家金融市場的了解。並且無論是自己投資或倚靠特定投資經理的協助,都應採取有紀律的投資計劃以保持在各種市場環境中的持續投資。

Mr. Cheng is a managing partner at Clarity Investment Partners, a Hong Kong based independent private investment office that directly manages personal accounts for families and institutions.

www.clarityinvestment.com

鄭先生為可承資本的董事合夥人。可承資本是一家總部設於香港,並專為高淨值家族及法人機構直接管理資產的獨立投資辦公室。

www.clarityinvestment.com/2002738913.html

● 讀後留言使用指南

|

近期迴響