|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

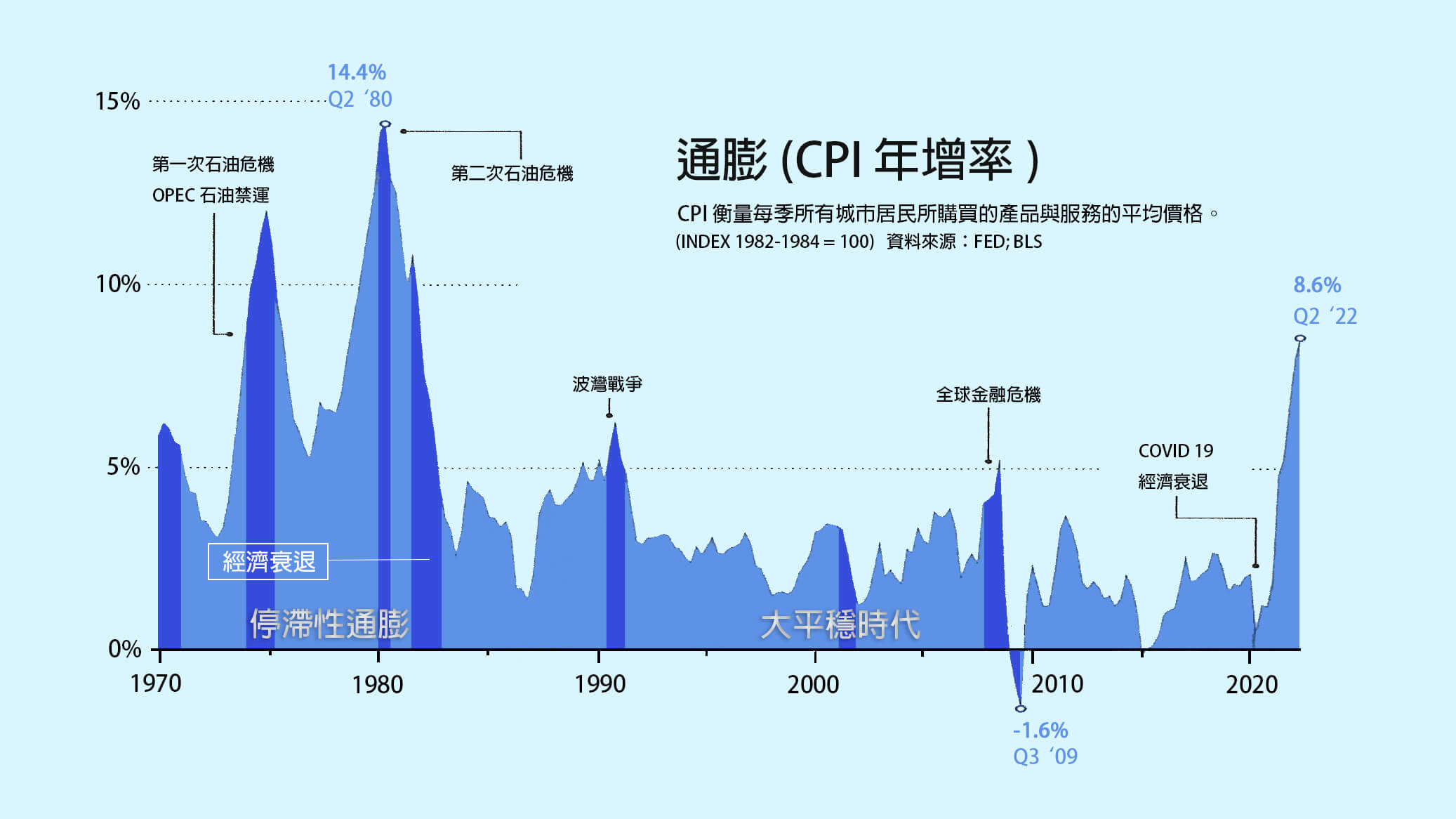

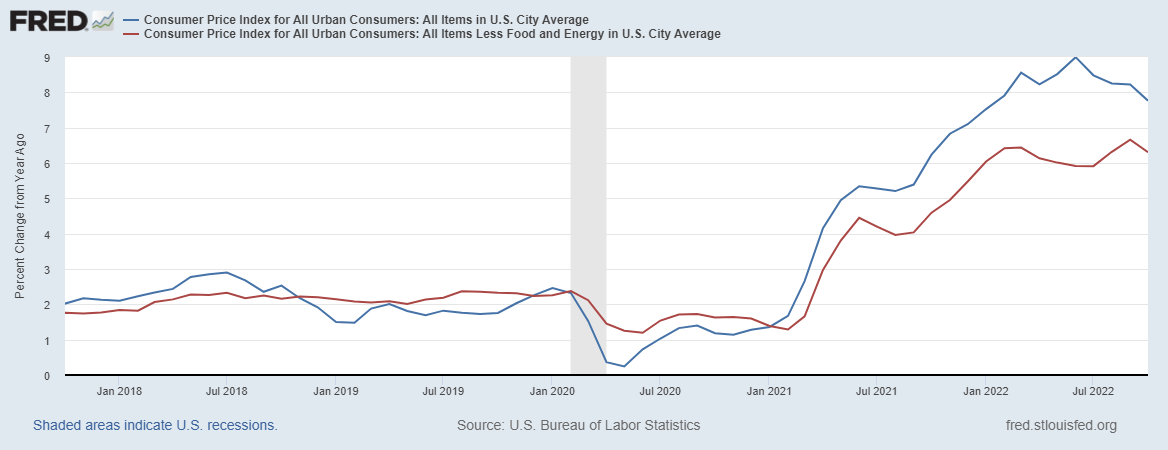

With markets ravaged this year by the prospects of high interest rates, particularly in the US, the November inflation data provided a welcome boost to equities. October US CPI rose 0.4% and Core CPI rose 0.3% vs consensus expectations of 0.7% and 0.5% respectively. Year over year, prices rose 7.7% versus 8.2% in the prior month. In response, the S&P 500 Index rallied 5.5% in a single day while the Nasdaq rose 7.4% and continued to rise in the following days. In Asia, where there was the additional positive development of easing quarantine restrictions in China, markets also rallied that day, with Hong Kong rising 7.7%, Japan rising nearly 3% and Korea rising over 3%. It remains to be seen if the trend also changes for inflation in other major economies in Asia and Europe.

由於今年市場一路受到高利率預期—尤其是美國–的打擊,11 月的通脹數據為股市提供了可喜的提振。 10月美國CPI上漲0.4%,核心CPI上漲0.3%,而市場普遍預期分別為0.7%和0.5%。 與去年同期相比,CPI值上漲了7.7%,而上個月該數據為8.2%。 作為回應,標準普爾500指數在一天內上漲了5.5%,而納斯達克指數上漲了7.4%,並在之後的幾日內繼續攀升。在亞洲,因中國放寬檢疫限制取得了額外的積極進展,當天股市上漲,港股漲7.7%,日本股市漲幅近3%,韓國股市上漲超過3%。亞洲和歐洲其他主要經濟體的通脹趨勢是否也會發生變化還有待觀察。

Going forward, it’s easy to see that market performance will be heavily dependent on economic data releases. After expectations reset for the next inflation print, whether US CPI surprises on the upside or downside will continue to have a significant impact on dollar rate expectations and financial returns. The good news is that in the latest release, core goods prices fell 0.4% while much of the core services increase was driven by rental inflation, of which leasing data shows has potentially peaked. On the other hand, it would not be realistic to assume a return to the low inflation days of the previous decade as global supply chains are undergoing a decoupling due to geopolitics.

展望未來,很容易看出市場表現將重度依賴於經濟數據的發佈。 在對下一次通脹數據進行預期重置後,無論美國CPI的上行或下行都將繼續對美元利率預期和財務回報產生重大影響。好消息是,在最新發布的數據中,核心商品價格下跌了0.4%,而大部分核心服務的增長是由租金通脹推動的,租賃數據顯示租金通脹可能已經見頂。 另一方面,認為經濟將回到過去十年的低通脹時期是不切實際的,因為全球供應鏈正在因地緣政治而脫鉤。

Is it the time to place a big bet based on the direction of the market and economy? Probably not, as it’s unclear to what extent the market is already discounting all the possible paths going forward. There are many problems inherent in investing based on macro bets and market timing, including the difficulty of trying to consistently predict the future, increased transaction costs, and increased opportunity costs. Furthermore, even when you call the right direction, it is risky to assume that your methodology was correct rather than being lucky in a coin flip, which could lead to large mistakes in the future.

那麼現在是根據市場和經濟方向下大賭注的時候了嗎? 可能不是,因為目前還不清楚市場已經在多大程度上折現了未來所有可能的走勢。 基於宏觀賭注和市場時機的投資存在許多固有問題,包括難以始終如一的預測未來、交易成本和機會成本的增加。此外,即使你的判斷是正確的,但是要就此認為你的方法論是正確的也是很危險的,即便猜中,也可能像投擲硬幣一樣純屬好運。 而這可能會導致將來出現重大錯誤。

Why then, do we spend so much focus on understanding the macro environment and impact on financial markets as investors if we’re not making big bets on them? Having a better understanding about what is moving prices is not as difficult a proposition as predicting what will happen in the future versus market expectations. As a thought experiment, imagine being blindfolded while the floor is moving strangely under you. Not knowing what is going on might lead you to want to escape whatever room you’re in. However, seeing that you are on a boat in the ocean is still valuable, even if you can’t predict what the waves or current will do. Seeing what is happening better prepares an investor to NOT react to market moves rather than being fearful over things affecting their portfolio that are hard to understand.

那麼,如果我們不對宏觀環境及其對金融市場的影響進行投注,為什麼還要花這麼多精力去瞭解宏觀環境以及其對金融市場的影響呢? 更好地瞭解價格背後的因素並不像預測未來與市場預期那麼困難。 作為一個思考實驗,想像一下被蒙住眼睛,而地板在你身下奇怪地移動。不知道發生了什麼可能會導致你想逃離你所在的任何房間。 然而,看到你正在一艘在海洋中的船上仍然很有價值,即使你無法預測海浪或洋流會做什麼。 更好地看到正在發生的事情並不是讓投資者擔心一些影響其投資組合的他們無法理解的事情,而是可以讓投資者做好準備,不要對市場動盪做出盲目反應。

Also, you want to make sure that your portfolio is prepared for the spread of realistic scenarios that could happen, rather than just one outcome. When equity indexes eventually do emerge from the 2022 bear market, this may give you the confidence you need to participate in the recovery.

此外,您希望確保您的投資組合為可能發生的一系列合理情況做好準備,而這將不會僅僅是一個結果。 當股票指數最終從 2022 年的熊市中走出來時,這 (準備) 可能會讓您有信心參與復甦中的投資。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation

【編者按】作者雖然強調宏觀數據對金融市場的影響,但不認為投資者就應概括目前宏觀情勢去做投資決策。 因為影響股市的還有其它複雜的因素,僅靠宏觀預測難以掌握。

● 讀後留言使用指南

|

近期迴響