|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

Causing a bit of market concern for investors in March, several banks in the US and Europe became financially distressed and required government intervention to prevent their problems from spreading throughout the financial system. While the situation is still unfolding, this is an opportunity for investors to evaluate the different kinds of risk exposures that they have in their portfolios and how to mitigate them.

3 月份,美國和歐洲的部分銀行陷入財務困境,需要政府的干預以防止它們的問題蔓延到整個金融體系,這引起了投資者的一些擔憂。 雖然情況仍在發展,但這是一個讓投資者評估其投資組合中不同類型風險敞口以及如何減輕這些風險的好機會。

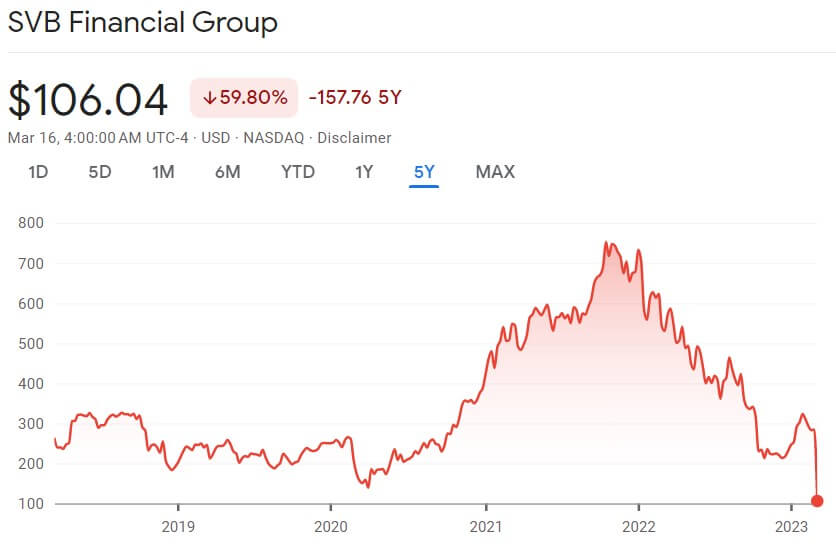

In the US, Silicon Valley Bank and Signature Bank (as well as the smaller Silvergate Bank) were forced to close, causing the US Federal Reserve to step in and guarantee the assets of their depositors to prevent any further panic. Silicon Valley Bank was notable due to its exposure to the tech and startup industry in the US, with high growth in accounts with deposits well in excess of the US 250,000 insured by the FDIC, which made it vulnerable to a bank run. As word spread of its financial troubles brought about by improper risk management and vulnerability to rising bond yields, depositors hurried to withdraw their cash which lead to even more withdrawals as fears spread. Meanwhile, both Silvergate Bank and Signature Bank had significant exposure to the struggling crypto currency industry and faced depositor withdrawals before being closed by regulators.

在美國,矽谷銀行、Signature Bank(以及規模較小的 Silvergate 銀行)被迫關閉,導緻美聯儲介入並為其儲戶的資產提供擔保,以防止進一步的恐慌。 矽谷銀行因其涉足美國科技和初創行業而引人注目,其存款賬戶的高速增長遠遠超過 FDIC 擔保的 250,000 美元,這使其容易受到銀行擠兌的影響。 由於不當的風險管理和債券收益率上升的脆弱性導致其財務問題的消息傳開,儲戶急於提取現金,並且隨著恐懼的蔓延,導致了更多儲戶的提款。 與此同時,Silvergate Bank 和 Signature Bank 都對陷入困境的加密貨幣行業有重大風險敞口,並在被監管機構關閉之前面臨儲戶提款問題。

矽谷銀行金融集團

Even more concerning, on March 14th, the Swiss giant, Credit Suisse reported that it had identified weaknesses in its own financial reporting and its share price dropped 25% after its investors declined to provide financial assistance. Being a global systemically important financial institution, the consequences of a potential failure would be dire for financial markets, but this reason also made intervention by the government much more likely. On March 16th, the Swiss central bank stepped in an provided USD 53.7 billion loan to strengthen Credit Suisse’s liquidity.

更令人擔憂的是,3 月 14 日,瑞士巨頭—瑞士信貸報告稱,它發現了自己財務報告中的弱點,在投資者拒絕提供財務援助後,其股價下跌了 25%。 作為一家具有全球系統重要性的金融機構,潛在倒閉的後果對金融市場來說將是極其可怕的。 而正因如此,使得政府干預的可能性更大。 3 月 16 日,瑞士央行介入提供了 537 億美元的貸款,以增強瑞信的流動性。

瑞信集團

Most investors so far have had minimal impact from these events. As of the time of writing, the effect on the global equity markets has been minimal, though if more banks are found to have been making the same mistakes in the rising rate environment, further turmoil might be down the road. This would be classified as a macro risk and a total market risk that is difficult to diversify away no matter what kind of stocks you held in your portfolio. For most people, it is not worthwhile to speculate on the direction of macroeconomic shocks as the timing of events is difficult to predict and furthermore, one would also have to accurately gauge the reaction of regulators. Certain specialized investors could potentially profit from making informed bets when markets overreact and they expect the government to step in, but again they need to have very good timing and a professional gambler’s temperament. For everyone else, it is better to have constructed their portfolios for a level of risk where they could avoid the temptation to trade around these kinds of events.

到目前為止,這些事件對於大多數投資者的影響微乎其微。 截至撰寫本文時,對全球股市的影響也微乎其微。 但如果之後有更多銀行在利率上升環境中犯同樣的錯誤,那麼未來可能會出現進一步動盪。 這將被歸類為宏觀風險和總體市場風險,無論您在投資組合中持有哪種股票,都難以分散此類風險。 對大多數人來說,宏觀經濟衝擊的走向不值得揣測,因為事件發生的時間點難以預測,而且還必須準確衡量監管機構的反應。 當市場反應過度並且他們期望政府介入時,某些專業投資者可能會從明智的賭注中獲利,但同樣他們需要有非常好的時機和專業賭徒的氣質。 對於其他人來說,最好是構建某一個風險水平的投資組合,這樣他們就可以避免圍繞此類事件進行交易的誘惑。

Now, if you were a shareholder in Silicon Valley Bank or one of the other ones, you are exposed to the idiosyncratic or specific risk of its stock. This kind of risk is mitigated by portfolio diversification. With the share price likely going to zero, if it was only a small percentage of your portfolio and you are not leveraged, you could take the loss without much trouble. Alternatively, if you had bet a large chunk of your portfolio on this company or if you took on a lot of industry specific risk to similar small banks, then this loss would be difficult to recover from.

那麼假設你是矽谷銀行或其他銀行的股東之一,你將會面臨其股票的特殊或特定風險。 投資組合多元化可以減輕這種風險。 隨著股價可能趨於零,如果它只佔您投資組合的一小部分並且您沒有使用槓桿,您可以毫不費力地承擔這樣的損失。 如果您將大部分投資組合押在這家公司上,或者如果您為類似的小銀行承擔了很多行業特定風險,那麼這種損失將很難彌補。

One more level of risk is counterparty risk. If you were a depositor in one of these institutions, particularly if your deposit level was above the $250,000 insured, there was a chance of loss in the event that regulators did not step in. Counterparty risk is also present in transactions like holding a structured product or off-exchange derivative at a trouble financial institution. Rationally, the thing to do in this situation is to move your assets elsewhere if you can, as soon as possible. There is little personal downside and significant savings in the event of total failure. While there is the moral question of contributing to a panic, this is more of issue for regulators to mitigate, both before and after the crisis. As long as you’re not actively trying to create such panic, and if you’re not a financial titan like JP Morgan in the 1920s, there is little that holding your personal deposits in these institutions could have done anyway by themselves.

更進一級的風險是交易對手風險。 如果您是這些機構之一的存款人,特別是如果您的存款水平高於 250,000 美元的受保額,那麼如果監管機構不介入,您就有可能遭受損失。 交易對手風險也存在於持有結構性產品等交易中或有問題的金融機構的場外衍生品。 理性地說,在這種情況下要做的是盡快將您的資產轉移到別處,因此當該機構出問題時,個人損失才會很小,而且可以節省大量資金。 儘管這麼做存在助長恐慌的道德問題,但這是監管機構在危機前後需要緩解的問題。 只要你不是積極地試圖製造這種恐慌,並且你不是類似 1920 年代摩根大通這樣的金融巨頭,那麼將你的個人存款存放在這些機構中本身就無關緊要。

Different types of risks require different reactions. If you moved your portfolio to cash every time there was a hint of macroeconomic weakness or systemic financial risk, your portfolio returns would fall significantly behind due to opportunity costs. On the other hand, if you find yourself too exposed to idiosyncratic, industry or counter party risk, immediate action may be warranted. In any event, it is always better to deal with your exposures and tolerance for risk before anything happens rather than in reaction to a crisis.

不同類型的風險需要作出不同的反應。 如果每次出現宏觀經濟疲軟或系統性金融風險跡象時,您都將投資組合轉為現金,您的投資組合回報將會因為巨大的機會成本而大大落後。 另一方面,如果您發現自己過於暴露於某些特殊風險、行業風險或交易對手風險,則可能需要立即採取行動。 無論如何,最好在任何事情發生之前處理好您的風險敞口和風險承受能力,而不只是針對危機做出反應。

圖說:Risk Management by Nick Youngson CC BY-SA 3.0 Pix4free.org

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation

● 讀後留言使用指南

|

近期迴響