|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

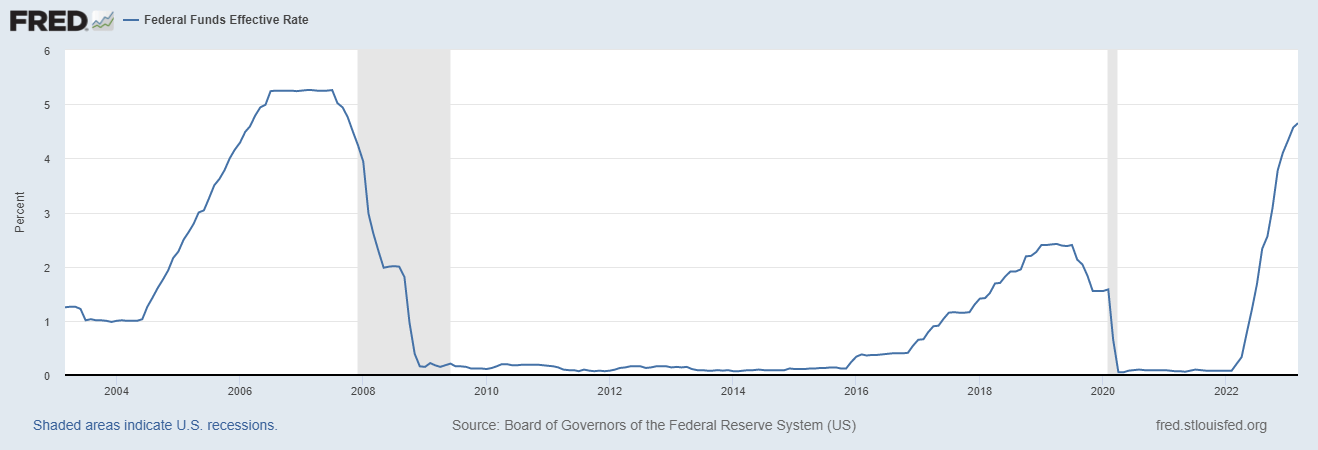

In March, the US Federal Reserve continued raising its key interest rate to the 5% level as part of its efforts to contain inflation. This was the ninth consecutive rate hike from the initial 0.25% level starting in March 2023 and slightly controversial due to the troubles at several US regional banks at the time. From the minutes of the FOMC (from March 21-22, released April 12), it appears that the Fed is beginning to soften its stance a little bit on how much more tightening “may be appropriate”. Going forward, it is not certain whether the Fed will continue to raise rates in May or pause, although the probability of a hike increased following the March jobs report which showed the US gained 236,000 jobs in the month. Regardless of what happens, it appears that we are coming closer to the end of this hiking cycle and investors may wonder whether it will also signal a change for the ongoing market recovery this year.

3 月份,美聯儲繼續將關鍵利率上調至 5% 水平,作為其遏制通脹的其中一個手段。 這是從 2023 年 3 月初始 0.25% 的水平後連續第 9 次加息,並且由於當時美國幾家地區性銀行的危機而略有爭議。 從聯邦公開市場委員會的會議紀要(3 月 21 日至 22 日,4 月 12 日發布)來看,美聯儲似乎開始稍微軟化其關於收緊“可能合適”的程度的立場。 展望未來,不確定美聯儲是否會在 5 月份繼續加息或暫停加息,儘管在 3 月份就業報告顯示美國當月增加 236,000 個就業崗位後加息的可能性增加。 無論發生什麼情況,我們似乎都在接近本次加息週期的尾聲,投資者們可能想知道這是否也預示著今年持續的市場復甦將發生變化。

During the initial stages of a rate hike cycle, the S&P 500 has historically experienced some volatility and declines. For example, during the last rate hike cycle from 2015 to 2018, the S&P 500 declined by approximately 10% in early 2016 and again in late 2018, both periods when the Federal Reserve was raising interest rates. However, as the rate hike cycle progresses and the economy adjusts to higher interest rates, the S&P 500 has historically recovered and even outperformed. During the same rate hike cycle from 2015 to 2018, the S&P 500 had an annualized return of approximately 8% despite the temporary declines.

在加息週期的初始階段,標準普爾 500 指數歷會經歷一些波動和下跌。 例如,在 2015 年至 2018 年的上一個加息週期中,標準普爾 500 指數在 2016 年初和 2018 年底分別下跌約 10%,而這兩個時期美聯儲都在加息。 然而,隨著加息週期的推進和經濟對更高利率的調整,標準普爾 500 指數會逐步複蘇,甚至跑贏歷史均值。 在 2015 年至 2018 年的同一加息週期中,標準普爾 500 指數的年化回報率約為 8%,儘管有時會出現短暫下跌。

Here are a few more examples of how the S&P 500 has performed during rate hike cycles:

以下是標準普爾 500 指數在加息週期中表現的更多示例:

2004-2006: The Federal Reserve raised interest rates from 1% to 5.25% over a two-year period from 2004 to 2006. During this time, the S&P 500 had an annualized return of approximately 11%, although there was some volatility during the period.

1999-2000: The Federal Reserve raised interest rates six times in 1999 and 2000, bringing the federal funds rate to 6.5%. During this time, the S&P 500 had a return of approximately 15%, although the dot-com bubble burst in 2000 and led to a significant decline in stock prices.

1994-1995: The Federal Reserve raised interest rates seven times from 1994 to 1995, bringing the federal funds rate from 3% to 6%. During this time, the S&P 500 also had a positive return (around 2%).

2004-2006:美聯儲在 2004 年至 2006 年的兩年時間裡將利率從 1% 上調至 5.25%。 在此期間,標準普爾 500 指數的年化回報率約為 11%,儘管期間存在一些波動 時期。

1999-2000:美聯儲在1999年和2000年六次加息,使聯邦基金利率達到6.5%。 在此期間,標準普爾 500 指數的回報率約為 15%,儘管 2000 年互聯網泡沫破滅並導致股價大幅下跌。

1994-1995:美聯儲從 1994 年到 1995 年七次加息,使聯邦基金利率從 3% 上升到 6%。 在此期間,標準普爾 500 指數也取得了正回報(約2%)。

While we can’t expect the future to always follow the same pattern, it’s notable that during all the recent rate hike cycles, equity markets gained ground. Furthermore, in all these cycles, markets performed well in the year following the final rate hike. So far during the current cycle, global equity markets are still negative in performance but recovering. The Global Dow Index, comprising 150 blue chip stocks from around the world, was down -0.66% over the past year but up 7.8% year to date as of April 17th. The US S&P 500 has not recovered as much off its lows, down -5.8% over the past year but up 8.2% year to date while European and Japanese markets already have 1-year positive returns.

雖然我們不能指望未來走勢總是遵循相同的模式,但值得注意的是,在最近的所有加息週期中,股市都在上漲。 此外,在所有這些週期中,市場在最後一次加息後的一年表現良好。 到目前為止,在當前週期中,全球股市的年回報仍為負數,但正在復蘇。 由全球 150 只藍籌股組成的全球道瓊斯指數在過去一年下跌了 0.66%,但截至 4 月 17 日,今年迄今上漲了 7.8%。 美國標準普爾 500 指數並未從低點反彈太多,過去一年下跌了 5.8%,但今年迄今上漲了 8.2%,而歐洲和日本市場已錄得 1 年的正回報。

Ultimately, future market performance as well as the rate hike path will depend on the trajectory of the real economy and whether growth might be derailed by factors such as a crisis or inflation. Investors should be on the lookout for times of trouble but otherwise should not expect the trend to break on its own or due to incremental rate decisions.

最終,未來的市場表現以及加息路徑將取決於實體經濟的軌跡以及增長是否會因危機或通脹等因素而脫軌。 投資者應留意出現波動的時刻,但不應指望市場趨勢會自行中斷或因利率的逐步調升而中斷。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響