|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

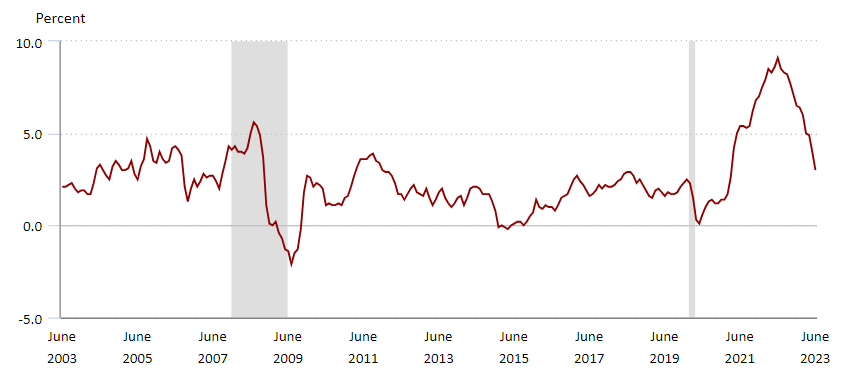

Inflation in the US continued to fall, hitting a two year low in June of 3% year over year and both equity and fixed income markets reacted positively to the data release. Going forward, the path of future rate decisions is uncertain, but investors are hopeful that inflation can continue to come down without requiring an economic downturn. With bond yields now at a more reasonable level after this recent hiking cycle, investors can now evaluate investing in various asset classes more fairly than when interest rates were near zero. As with most investment strategies, multi-asset investing styles depend on personal circumstances and preferences, and we will examine which may be best for different types of investors.

美國通脹率繼續下降,6 月份同比跌至 3%,創兩年新低,股票和固定收益市場也對該數據的發布做出了正向反應。 展望未來,未來利率決策的路徑尚不確定,但投資者希望在不發生經濟衰退的情況下通脹率能夠繼續下降。在最近的加息週期之後,債券殖利率現在處於更合理的水平,投資者現在可以比在利率接近於零時更公平地評估各種資產類別的投資。與大多數投資策略一樣,多元化資產投資風格取決於個人情況和偏好,我們將研究哪種投資策略最適合不同類型的投資者。

Source: US Bureau of Labor Statistics

來源:美國勞工統計局

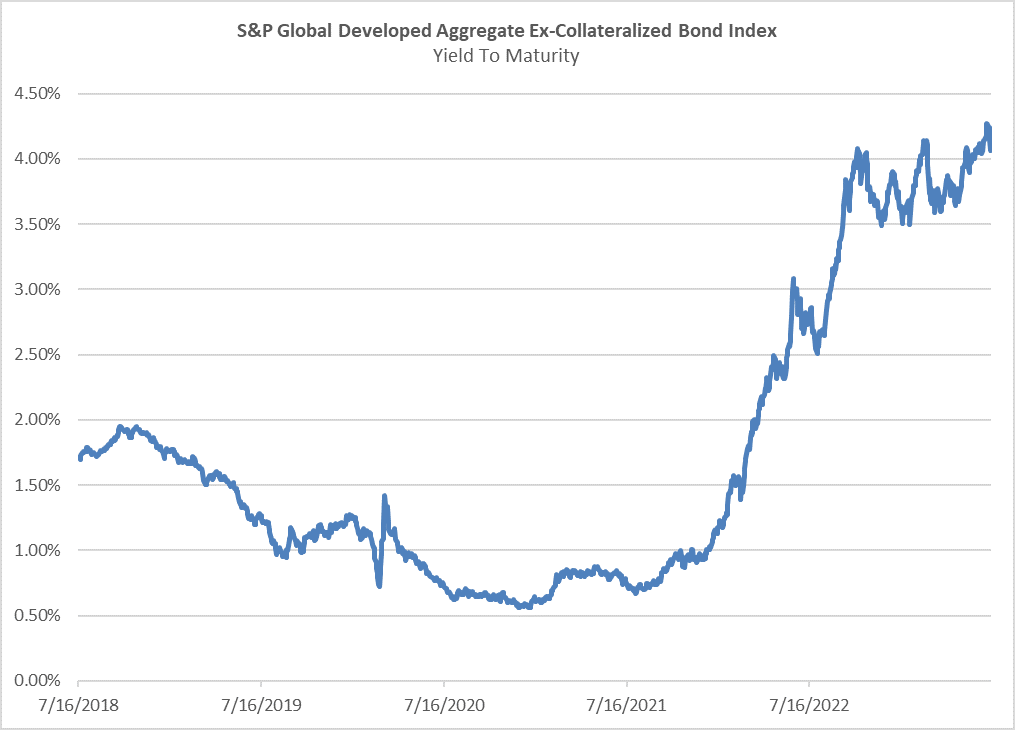

After the encouraging inflation data release, the yield curve, while still inverted, flattened as short-term bonds rallied. Nonetheless, markets are still pricing in a further 25 basis point hike from the Federal Reserve before the end of the year, as much of the fall in inflation has been driven by falling energy prices and core inflation is still higher year over year at 4.8%. Between the extremes of a potential future recession and a resurgence of inflation, are the possibilities of rates gradually coming down, or remaining at this level for the foreseeable future. Either way, bond yields are more reasonable for investors now than their levels over the past decade. Furthermore, as it is possible that inflation will continue to remain at elevated levels compared to the past, commodities may also be an attractive option for investors as protection against potential price spikes. Under certain market conditions going forward, a diversified multi-asset portfolio could outperform an equity + cash portfolio.

在令人鼓舞的通脹數據發布後,殖利率曲線雖然仍倒掛,但隨著短期債券上漲而趨平。 儘管如此,市場仍預計美聯儲將在年底前進一步加息 25 個基點,因為通脹下降的主要原因是能源價格下跌,而核心通脹率仍較去年同期更高,達到 4.8% 。 在未來潛在的經濟衰退和通脹復甦的兩極之間,比較可能的情況是利率有可能逐漸下降,或在可預見的未來保持在這一水平。 不管怎樣,對於投資者來說,現在的債券殖利率比過去十年的水平更加合理。 此外,由於通脹有可能繼續維持在較過去較高的水平,大宗商品也可能對投資者來說是一個有吸引力的選擇,用以防範潛在的價格飆升。在未來的某些市場條件下,多元化資產投資組合可能會優於股票+現金的投資組合。

Source: S&P

來源:標準普爾

Some investors will try to time the market aggressively, shifting between asset classes depending on their view of the market going forward. This is very difficult to execute, as even if the analysis and rationale is correct, the market may not react in a consistent manner in terms of timing. Many investors will pick a preferred asset class, such as equities, and allocate between it and cash depending on how aggressive or defensive they want to be. For an investor with skills and advantages in a single asset class, this might be the best strategy for them. A problem may come when there are fewer opportunities in that asset class, such as when market valuations are high, which then requires incredible discipline and patience on the part of the investor. Traditional asset allocation methods involve determining one’s risk tolerance and then picking a fixed percentage of asset classes to invest in depending on their historical volatility and correlations. This also has the problem of ignoring the investment opportunity set available which may favor one asset significantly over another.

一些投資者會激進地嘗試把握市場時機,根據他們對未來市場的看法在投資的資產類別之間轉換。 然而這卻是很難執行的,因為即使分析和理由是正確的,市場在時間上也可能以不一致的方式做出反應。 許多投資者會選擇一種偏愛的資產類別,例如股票,並根據他們想要的激進程度或防禦程度在資產類別和現金之間進行分配。 對於在單一資產類別中擁有技能和優勢的投資者來說,這可能是他們的最佳策略。 當該資產類別的機會較少時,例如當市場估值較高時,可能會出現問題。 傳統的資產配置方法需要投資者擁有難以置信的紀律和耐心以及風險承受能力,然後根據其歷史波動性和相關性選擇固定百分比的資產類別進行投資。 這還存在另一個問題就是可能會忽視一些可投資機會,這些投資機會可能是特別著重於某一種類型的資產。

Another logical method of asset allocation has its roots in academic finance theory. Based on the available opportunities, an investor can try to put together the most efficient set of assets based on their estimates of risk and return and then lever their portfolio up or down depending on their risk tolerance. While in theory, this would be a mechanical exercise based on precise estimates, in practice, the asset mix is more likely gradually accumulated as opportunities arise and estimating potential risks and returns is more of an art than a science. Furthermore, using leverage by buying securities on margin comes with its own set of dangers, as sudden market movements can force investors to sell at the worst times. Alternatively, if an investor usually keeps their liquid investment portfolio separate from their other assets including bank deposits and properties, they could then scale the size of their entire investment portfolio up or down in relation to their overall assets according to how much more or less risk they want to take.

資產配置的另一種符合邏輯的方法源於學術金融理論。 根據可用的機會,投資者可以嘗試根據他們對風險和回報的估計來配置最有效的資產組合,然後根據他們的風險承受能力提高或降低他們的投資組合。雖然從理論上講,這將是一種基於精確估計的機械操作,但在實踐中,隨著機會的出現,資產組合更有可能逐漸積累,並且估計潛在風險和回報更多的時候是一門藝術而不是一門科學。 此外,通過保證金購買證券來使用槓桿也有其自身的一系列危險,因為突發的市場波動可能會使投資者在最糟糕的時候被迫出售。 或者,如果投資者通常將其流動性投資組合與其他資產(包括銀行存款和房地產)分開,那麼他們可以根據想要承擔的風險水平來擴大或縮小其投資組合的規模。

Most importantly, implementing a multi-asset portfolio strategy requires understanding of the behavior under different market environments of each of the asset classes invested in, whether from one’s own knowledge or through an advisor. Also, the strategy should be undertaken with the objective of being robust through several different market cycles rather than just the one right in front of you.

最重要的是,實施多元資產投資組合策略時,無論是通過自身的知識儲備還是通過投資顧問,都需要了解所投資的每種資產類別在不同市場環境下的表現。 此外,採取這一策略的目標應該是在幾個不同的市場週期中都使投資組合保持穩健,而不只是眼前的一個投資週期。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響