|

| For a Better Tunghai |

|

| For a Better Tunghai |

by Charles Cheng, CFA

It makes sense that most investors prefer to make the bulk of their investments in their home region given various factors such as ease of access, understanding of local companies and regulations, and not having to make currency conversions. However, this is at odds with finance theory which holds that for most investors, it would be efficient for their portfolio allocation to be geographically weighted in proportion to global market capitalization. Should most investors be diversifying more globally?

大多數投資者更願意將大部分投資放在自己的家鄉地區進行。 考慮到交通便利性、對當地公司和法規的了解以及無需進行貨幣兌換等多種因素,這麼做是合理的。 然而,這與金融理論是相矛盾的。 金融理論認為,對於大多數投資者來說,他們的投資組合配置需要按照全球市值的比例進行地理加權才是有效的。 那麼大多數投資者是否應該在全球範圍內更加多元化?

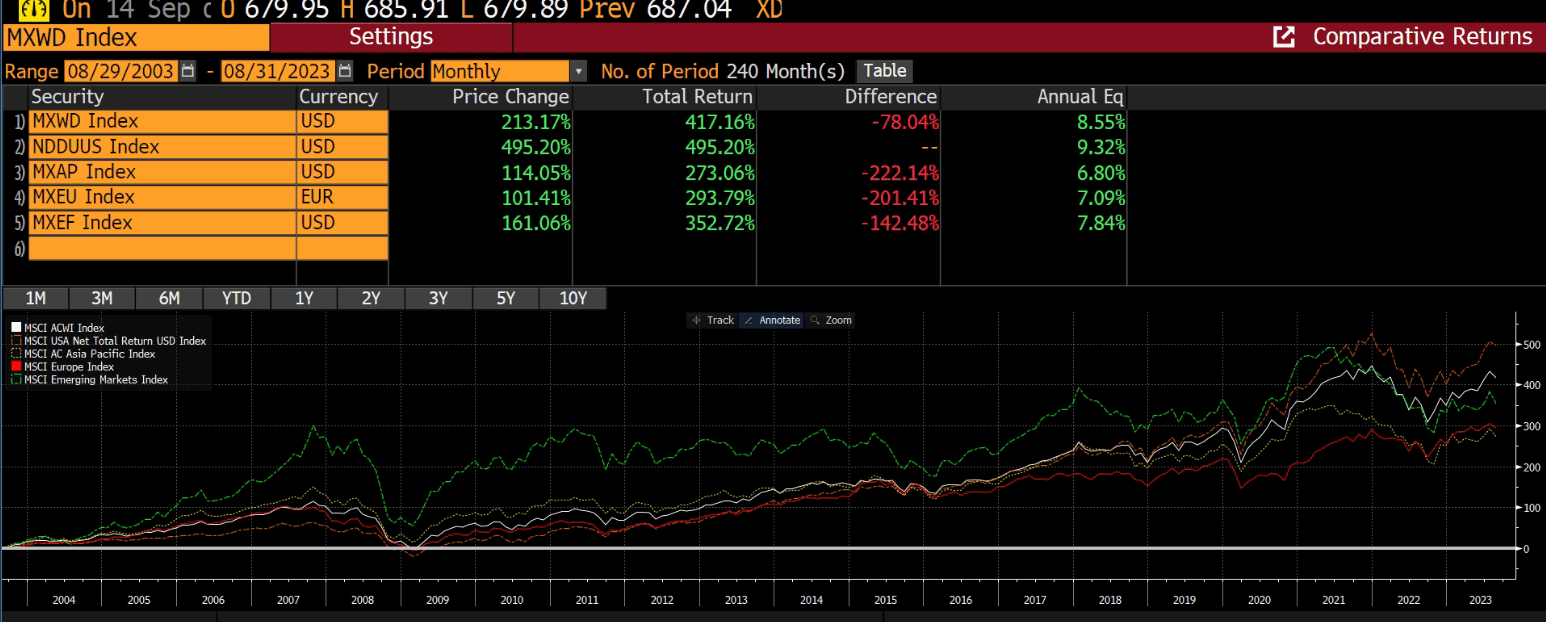

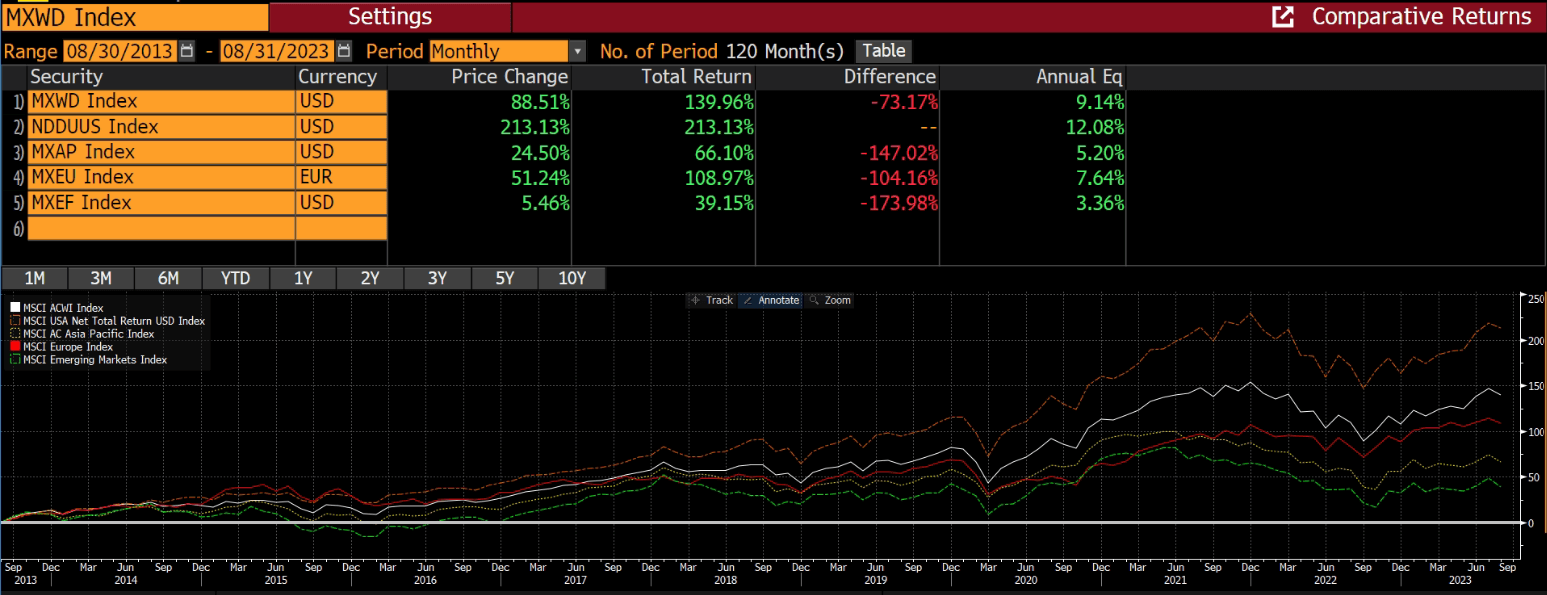

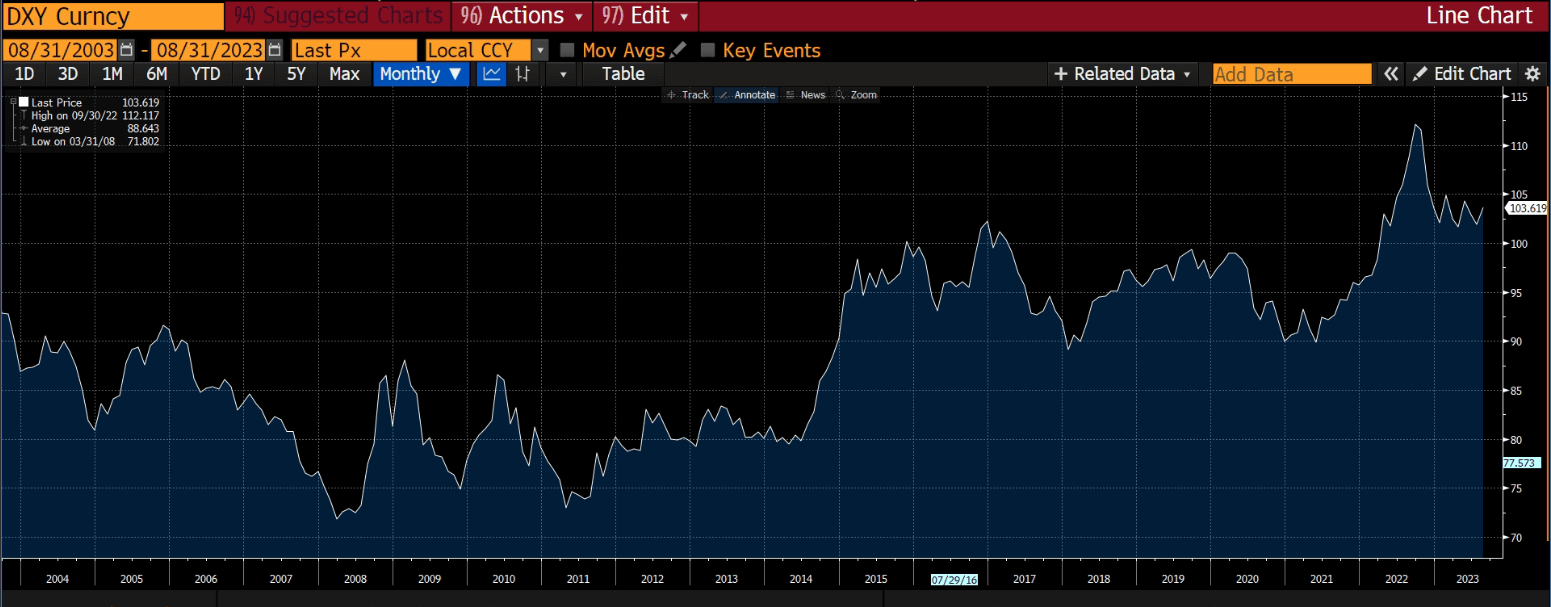

For the past five, ten, and even twenty years up to August 31st, 2023, the US equity market has outperformed the global benchmark and its various regional subindices significantly. On a twenty-year period, the MSCI US index returned 495.2% versus 417.16% for the MSCI All Country World Index. Over the past ten years, the difference is even more stark, at 213.1% vs 139.96%. Furthermore, the USD strengthened against an index basket of currencies over the same time period. This is hindsight of course, and past performance should not be expected as future returns. However, it’s worth noting that if you blindly held the global equity portfolio, the US would have been your largest country allocation, at roughly half the size of the global investible equity universe.

截至2023年8月31日的過去五年、十年甚至二十年裡,美國股市的表現顯著優於全球基準及其他各個區域的分類指數。 以過去20 年為例,MSCI 美國指數的回報率為 495.2%,而 MSCI 所有國家世界指數的回報率為 417.16%。 而過去十年的差異更加明顯,分別為 213.1% 和 139.96%。 此外,同期美元兌一籃子貨幣指數走強。 當然,這畢竟是事後諸葛亮,我們不應將過去的表現直接視為未來的回報。 然而,值得注意的是,如果你盲目持有全球股票投資組合,美國將也是你最大的配置國,其規模大約是全球可投資股票領域的一半。

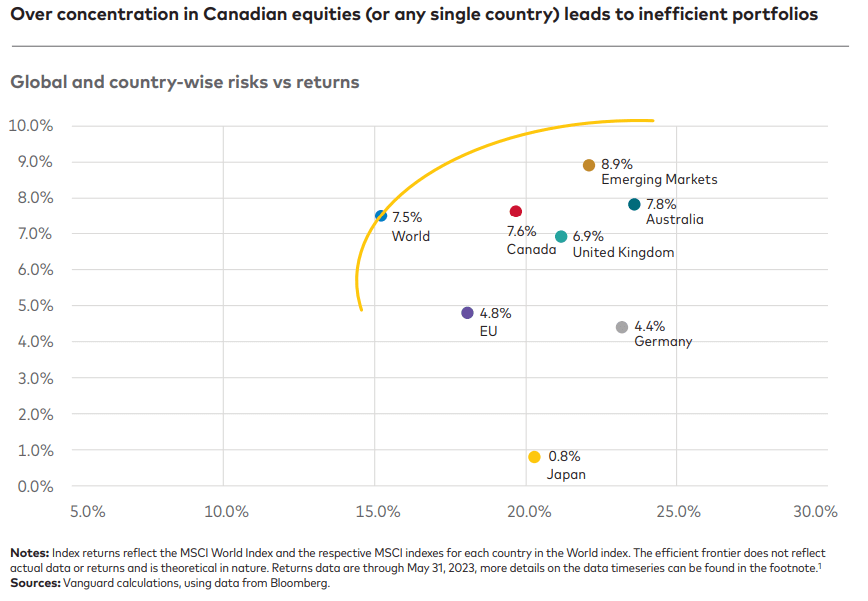

A recent report by Vanguard showed that Canadian investors allocated 52.2% of their equity portfolios to Canadian stocks while Canada only made up 3.4% of the global equity market. They estimated that the Canadian market returned around the same as the global market over the past 35 years but at around 25% higher risk as measured by standard deviation. Also, having the home country bias left its investors heavily exposed to the energy and financial sectors and underinvested in the technology industry. Despite the good reasons that Canadian investors may have had to be so highly weighted toward their own country, most would have likely benefited tilting their portfolios a bit more toward the global market allocation.

Vanguard最近的一份報告顯示,加拿大投資者將其股票投資組合的52.2%配置為加拿大股票,而加拿大僅佔全球股票市場的3.4%。 他們估計,過去 35 年加拿大市場的回報率與全球市場大致相同,但按標準差衡量,風險高出約 25%。 此外,母國偏見導致投資者過多投資於能源和金融行業,而對科技行業的投資不足。 儘管加拿大投資者可能不得不如此高度重視自己的國家,但大多數人如果將他們的投資組合更多地向全球市場配置傾斜,那麼他們可能會受益更多。

Source: Vanguard

來源:領航投資

Also, while investors would be more familiar and comfortable with their local country risks, they are also doubling down on those risks with their portfolio, with their own jobs and businesses likely linked to the domestic economy and exposed to the same risk factors such as political and foreign exchange. While it may be going too far to say that the global market portfolio is the most efficient, all else being equal, it is an allocation that is well diversified, highly liquid, and weighted toward large winning companies, and would serve as a good starting point when looking to allocated internationally. As technology and large financial platforms make it easier and easier to invest outside of investors’ home regions cheaply, we should expect to continue to see individual portfolio allocations go more global.

此外,雖然投資者對本國風險更加熟悉和放心,但他們的投資組合所承擔的風險也會加倍。 因為他們自己的工作和企業可能都與國內經濟相關,並面臨政治、外匯等相同的風險因素。 雖然在其他條件相同的情況下,說全球市場投資組合是最有效的可能有些言過其實,但它是一種多元化、流動性高、偏重於大型成功企業的配置,作為尋求國際化配置時不失為一個良好的開端。 隨著技術和大型金融平台使得在投資者所在地區以外進行平價投資變得越來越容易,我們應該期望繼續看到個人投資組合配置更加全球化。

This article reflects the personal views of the author and not any firm’s and should not be viewed as an investment recommendation.

● 讀後留言使用指南

|

近期迴響